Confidential Offering · Opportunity Zone · 2026

Hustead

House

302 beds. 0.3 miles to UC Berkeley.

A fully-entitled, purpose-built student housing development in one of America's most supply-constrained university markets — sited within a federally designated Opportunity Zone.

Yield on Cost

6.62%

+212 bps vs market cap

Total Project Cost

$56.2M

$760K / unit

Stabilized NOI

$3.73M

Year 1 stabilized

Stabilized Value

$82.8M

@ 4.50% cap

LP IRR

26.0%

2.86x equity multiple

Avg Rent / Bed

$1,554

Below all benchmarks

Executive Summary

The case for Hustead House is structural, not cyclical.

Berkeley is undersupplied by ~3,949 beds at the subject's 2028 delivery window — even after fully crediting every committed delivery. Each academic year resets a recurring leasing engine of 46,000+ students. The shortfall does not close.

01 · Demand

Structural undersupply

UC Berkeley enrollment exceeds 46,000 with durable ~2% annual growth. Only ~25% can be housed on campus. Strict zoning and 4–6 year entitlement timelines have constrained off-campus supply formation. Even fully credited through 2030, the campus-proximate market remains undersupplied.

02 · Position

Best-in-class infill location

Steps from UC Berkeley’s southern boundary at 0.3 miles. Walk Score 99, Bike Score 98. Two BART stations within a mile. The Telegraph corridor is the highest-trafficked student retail node in the East Bay — and the subject is mid-block on it.

03 · Returns

6.62% yield on cost, 212 bps spread

Total project cost of $56.2M produces $3.73M stabilized NOI — a 6.62% yield on cost with a 212 bps spread to a conservative 4.50% exit cap. LP returns target 26.0% IRR / 2.86x equity multiple over a 5-year hold.

04 · Tax

Opportunity Zone advantage

Federally designated Qualified Opportunity Zone (tract CA 4235.02). Capital gains deferral via QOF investment; 100% federal tax exemption on appreciation if held 10+ years. Materially enhances after-tax economics for institutional LPs deploying capital gains.

Market Dynamics

A flagship public university producing recurring demand against a development pipeline that cannot keep up.

46,151

UC Berkeley Enrollment

Fall 2025 · +22.8% over decade

24.7%

On-Campus Coverage

11,333 beds · structurally capped

3,949

Bed Shortfall

Campus-proximate · 2028 delivery

1,776

Shortfall — 2030

Fully-credited downside · still open

The Demand Side

UC Berkeley grew ~28% over the prior decade and proved resilient through COVID. Only ~25% of students can be housed on campus — even after People's Park (2027) and 2200 Bancroft (2030) deliver, off-campus dependency stays permanent. Each academic year resets the leasing engine.

The Supply Side

Berkeley does not produce continuous PBSH supply. Projects cluster in discrete waves separated by extended quiet periods. The 2028–2030 pipeline is highly visible and finite. Subject delivers into the structurally undersupplied 2028 window.

Location & Connectivity

Proximity

- 0.3 mi

UC Berkeley Campus

5 min walk · 2 min bike

- 99 / 98

Walk / Bike Score

Walker's Paradise

- 0.5 mi

Downtown Berkeley BART

10 min walk · 3 min bike

Site Transformation

Drag to compare existing condition vs. proposed development

Project Overview

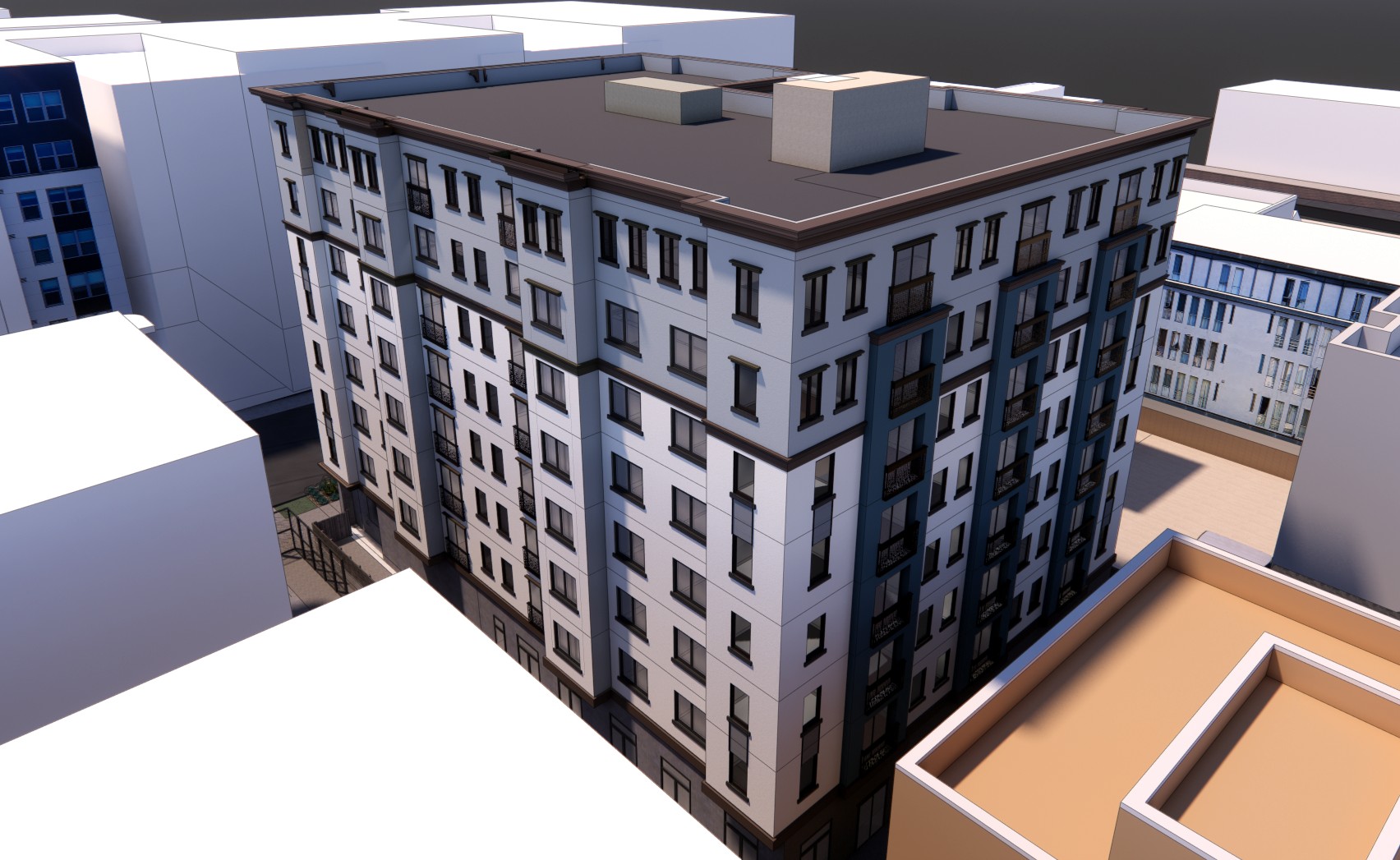

74 units. 302 beds. 8 stories. Designed for the campus-adjacent renter.

Building Program

| Residential Units | 74 |

| Total Beds | 302 |

| Beds / Unit (avg) | 4.08 |

| Total GSF | 76,800 SF |

| Net Residential SF | 58,287 SF |

| Ground-Floor Retail | 1,600 SF |

| Net-to-Gross | 75.9% |

Site & Construction

| Site Area | 12,501 SF |

| Stories | 8 |

| Zoning | C-DMU Buffer |

| Construction Type | IA / IIIA |

| Parking | Transit-oriented · zero req. |

| Entitlements | Fully entitled |

| Opportunity Zone | Qualified (Tract CA 4235.02) |

Design & Architecture

Project Visualization

Unit Mix

14 model unit types aggregated into 4 public categories · sample rent shown per category

| Type | Units | Beds | Beds / Unit | Avg SF | Sample $ / Bed |

|---|---|---|---|---|---|

| Studio | 1 | 1 | 1.0 | 351 | $3,200 |

| 2 Bedroom | 10 | 20 | 2.0 | 505 | $2,350 |

| 3 Bedroom | 59 | 265 | 4.5 | 760 | $1,715 |

| 4 Bedroom | 4 | 16 | 4.0 | 876 | $2,200 |

| Total | 74 | 302 | 4.08 | — | $1,554 blend |

Unit Design & Living Experience

Representative Floor Plans

Studio

1 Bed / 1 Bath · 351 SF

$3,200/bed

2 Bedroom

2 Bed / 1 Bath · 505 SF

$2,350/bed

3 Bedroom

3 Bed / 1.5 Bath · 760 SF

$1,715/bed

4 Bedroom

4 Bed / 2 Bath · 876 SF

$2,200/bedIn-Unit Laundry

Washer/dryer in every unit

Smart Entry

Keyless access throughout

High-Speed Internet

Fiber internet included

Full Kitchens

Stainless steel appliances

Floor-to-Ceiling Glass

Maximizing natural light

Luxury Vinyl Plank

Premium flooring

Quartz Countertops

Modern cabinetry

Energy Efficient

Sustainable fixtures

Business Plan

Milestones tied to model: Jan 2027 construction start · 18-month build · 3-month stabilization

Now – Q3 2026

Permitting & Final CDs

Finalize construction documents from 75% to 100%. Building permit target Sep 2026 (ministerial).

Q4 2026

Site Preparation

Demolition of existing single-story commercial structure. Foundation work and site mobilization.

Q1 2027 – Q2 2028

Vertical Construction

18-month construction per West Builders GMP. Type IA/IIIA · 8-story mixed-use.

Q1 – Q3 2028

Pre-Leasing

Pre-leasing begins ~6 months before delivery. Target Fall 2028 academic year move-in.

Q4 2028 – Q1 2029

Stabilization

95%+ occupancy through first academic semester. Korean café opens at ground floor.

Financial Profile

The numbers. Tied live to the financial model on this site.

Project Yield on Cost

6.62%

212 bps spread to 4.50% market cap

LP Pre-Tax IRR

26.0%

2.86x equity multiple · 5-yr hold

Stabilized Value

$82.8M

$274K / bed @ 4.50% cap

Stabilized NOI

$3.73M

Year 1

Total Project Cost

$56.2M

$760K / unit

Stabilized Value

$82.8M

@ 4.50% cap

Total Debt

$44.0M

76.7% LTC · 1.30x DSCR

LP Equity

$6.75M

Class A · 8% pref

All figures sourced from the live financial model on this site

View detailed returns →Capitalization

Sources

Uses

Sponsor & Team

Jonathan Yi

Project Sponsor

Former high-tech product manager. Licensed real estate professional. Over 25 years of entrepreneurial leadership in business development and real estate ventures.

Janice Lee

Project Sponsor

Former stockbroker with Series 7 license. Experience at PaineWebber and Thomas Weisel Partners. Licensed real estate professional since 2004.

Aran Kaufer

Construction Manager

Licensed architect with 27+ years in multifamily residential construction, primarily in Berkeley. Expert in local permitting and housing development.

Chris Porto

Development Manager

Real estate development entrepreneur with 10+ years experience. Former Deloitte consultant. Capital advisory expertise across construction loans, preferred equity, and JV equity.

General Contractor — West Builders

West Builders has built more than 50% of all new construction projects in Berkeley. Led by Ricardo Zamorano (President) and Dave de Jong (VP, Pre Construction).

Property Manager — Asset Living

Currently managing two new lease-ups in Berkeley. Engaged to generate the operating pro forma.

Key Risks & Mitigants

Construction Cost Escalation

GMP contract with West Builders. Construction documents 75% complete with active value engineering.

Entitlement & Permitting

Fully entitled with all discretionary approvals secured. Building permit targets late September 2026.

Lease-Up & Occupancy

Severe structural undersupply with ~4,000 bed shortage projected by 2028. Asset Living engaged with two active Berkeley lease-ups.

Capital Markets Environment

Construction loan committed at 69.3% LTC; agency permanent at 78.2% LTC sized to 1.30x stabilized DSCR (52.0% LTV at exit — LTV-bound, not cash-flow-bound). OZ equity structure provides built-in tax incentive independent of rate environment.

Investor Portal

Open the live

financial model.

Every figure on this page is sourced from the financial model in the investor portal. Move sliders. Run scenarios. Stress-test the assumptions. The numbers don't hide.